The root of growth and success of every business, small or big, often lies in the management of cash. Financial management is an indispensable tool that streamlines cash flow management and tax considerations. This is where cash accounting proves to be of utmost importance in business finance and accounting. It allows business owners to understand their expenses and receivables better.

Cash accounting records financial transactions only when cash is received or paid. This reliable accounting method facilitates decision-making and financial planning. Cash basis accounting, alternatively referred to as cash accounting, is most suitable for new startups and small businesses that conduct simple transactions. It simplifies accounting by exclusively considering cash inflows and outflows. Here are the insights into cash accounting and terms that will help you understand and implement this accounting method effectively.

Significance of cash accounting for business owners and entrepreneurs

Cash accounting is a method that records financial transactions exclusively upon the receipt or disbursement of physical currency. Stated it monitors the real-time cash movement that enters and leaves your company. Unlike accrual accounting, cash accounting does not account for pending invoices or unpaid bills. It keeps the accounts simple by focusing just on cash on hand - money collected directly from clients or paid to suppliers and vendors. It makes cash accounting very straightforward for business owners to understand and manage.

Due to the accounting system's reliance on real cash transactions, the financial statements produced—including cash flow statements, cash receipts, and cash payments—faithfully represent the company's actual liquid cash position. It provides entrepreneurs with a constant and transparent view of the financial position and liquidity of the business. Cash accounting simplifies maintaining records for small businesses that conduct less complex operations. It ensures the records are consistently updated to reflect the actual cash flow of the organization.

Common terms used in cash accounting business owners must know

Businesses use cash accounting to record income and costs as they receive or make payments. It simply records transactions when money exchanges hands, regardless of when they were begun. For example, if a company sells a product on credit, under the cash accounting system, the sales revenue is recorded after payment is received. To effectively manage cash flow, every entrepreneur must possess a fundamental understanding of specific cash accounting terms:

- Cash inflows: It refers to the cash a business receives from services, sales, or other sources of revenue. Cash inflow tracking assists companies in understanding their revenue streams.

- Cash outflows: It consists of all cash expenditures, including those for supplies, wages, rent, and utilities. Keeping track of outflows is crucial for budgeting and expenditure purposes.

- Cash balance: Deducting the total cash inflows from the total cash outflows yields the net balance. An updated cash balance reflects a company's actual amount of liquid funds.

- Cash basis: It entails documenting transactions solely upon the physical receipt or payment of cash, as stated previously, instead of using accrual. This notion forms the foundation of currency accounting.

- Cash equivalents: These are exceptionally liquid assets, such as money market funds or bank deposits, which can be instantly converted into cash with minimal risk.

Entrepreneurs can make more informed financial decisions as they understand the daily cash accounting reports with the help of this information. Accurate monitoring and documentation of currency inflows, outflows, and balances are imperative for companies to oversee their working capital needs and daily activities efficiently.

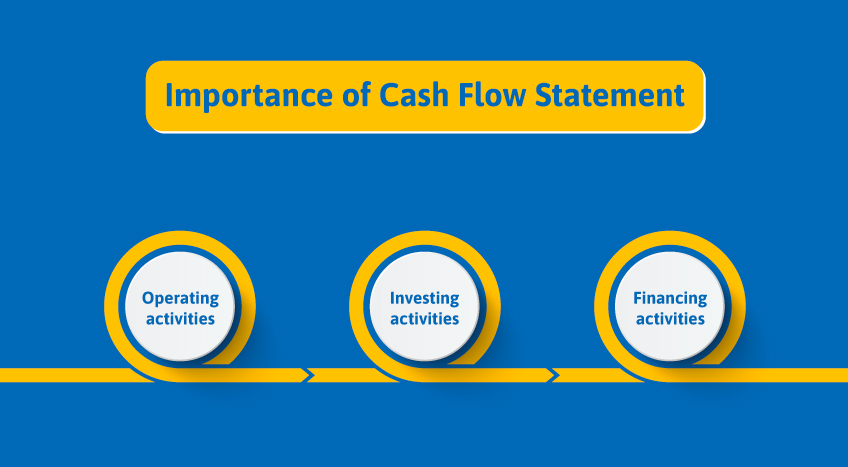

Importance of cash flow statement in business accounting

The Cash Flow Statement is a vital financial document for cash accounting companies. It summarizes the inflows and outflows of cash and cash equivalents within the company over the course of a given accounting period. Cash inflows and outflows are analyzed and classified into three fundamental activities—operating, investing, and financing—on a cash flow statement. It provides owners with a thorough look into the origins and uses of their funds.

- Operating activities: Cash transactions pertaining to the central business, such as payments to suppliers and cash received from consumers, are addressed in this section. It monitors the net cash flow produced by routine sales and expense operations.

- Investing activities: This consists of cash flows generated by the sale or purchase of property, plant, equipment, and other investments. It indicates the amount of cash generated or utilized for capital expenditures.

- Financing activities: This section addresses cash flows to and from financing sources, such as share issuance, taking loans, and debt repayment. It represents the net cash flow generated by financing activities.

Entrepreneurs can utilize the Cash Flow Statement as a valuable instrument to assess the origins and destinations of cash, determine the level of liquidity, appraise profitability, and strategize for forthcoming cash requirements essential for the business's efficient operation. It offers a comprehensive assessment of whether the operational activities of the business are yielding adequate cash flows.

Example of cash accounting in action

Let's examine the operation of currency accounting using an example. Consider a bakery business - Cupcakes 'n' More.

In the first week:

- Cupcakes 'n' More was paid in cash to sell cupcakes valued at Rs.10,000.

- It paid cash for the procurement of ingredients worth Rs. 5,000.

What is the procedure for recording this in financial accounting?

- As cash was acquired through sales, a cash inflow of Rs.10,000 will be documented.

- The ingredients' Rs. 5,000 cash payment will be documented as a cash outflow.

- Net cash balance after the first week = Rs. 10,000 (inflow) - Rs. 5,000 (outflow) = Rs. 5,000

In the second week:

- Sales were Rs. 8,000, but Rs. 2,000 has yet to be received.

- A salary of Rs. 3,000 was paid.

Under cash accounting, only cash transactions are considered. So:

- A cash inflow of Rs. 8,000 was generated due to executed sales.

- Cash outflow of Rs. 3,000 for wages.

- Net cash balance after second week = Rs. 5,000 (previous) + Rs. 8,000 - Rs. 3,000 = Rs. 10,000

It demonstrates that cash accounting is predicated on recognizing actual cash transactions, unlike accrual accounting, which records delinquent sales and liabilities. This method of monitoring cash flows enables companies to manage their liquidity effectively.

Final takeaways, grow your business with all-inclusive accounting tool TallyPrime

Cash accounting is a straightforward and efficient accounting method for managing the finances of small businesses. It gives business owners an insight into their company's liquidity while minimizing legal responsibilities by concentrating solely on actual cash inflows and outflows. As companies expand and their transactions become more intricate, accrual accounting is more suitable for representing accurate financial status.

Tally Solutions assists you in the maintenance of accounting records. The cash accounting module of Tally facilitates the streamlining of all cash-based accounting procedures. Automating daily accounting tasks and compliances, including invoicing, monitoring cash inflows and disbursements, and generating reports and statements such as Receipts, Payments, and Cash Flow, Tally facilitates these functions. Additionally, its integration with the GST ensures businesses remain current on tax compliance.